{kind=link}

Let me tell you something I wish someone had told me when I was 19 and signing for my first student loan: just because you’re studying finance doesn’t mean you automatically make good financial decisions for yourself. Ironic, right?

I spent 8 years working in student loan services before launching my own financial advisory practice, and I’ve seen countless finance majors graduate with debt portfolios that would make their professors cringe. Despite understanding the theory, many students fail to apply sound educational debt management strategy to their own situations.

Today, I’m sharing the exact loan analysis framework I’ve developed over 12 years of helping students optimize their educational financing. This isn’t theoretical—it’s battle-tested with hundreds of real students who’ve saved thousands in unnecessary interest and fees.

Why Even Finance Students Struggle with Educational Debt Management Strategy

Back in 2019, I met with a brilliant finance major named Marcus who had a 3.9 GPA and multiple job offers from prestigious firms. On paper, he was doing everything right. But when we sat down to review his loan portfolio, I discovered he had taken out five different loans at varying interest rates without any coherent strategy. He was on track to pay over $22,000 in unnecessary interest over the life of his loans.

“But I understand compound interest!” he protested, looking embarrassed.

Understanding concepts and applying them to your own life are completely different skills. Trust me, I learned this the hard way during my twenties when I was teaching financial literacy workshops while still carrying high-interest debt myself. God, I hate admitting that.

The truth is, most finance programs teach you how to manage corporate debt and investments, not how to optimize your personal educational debt management strategy. They rarely cover the nitty-gritty details of federal versus private loan options, income-driven repayment plans, or loan forgiveness programs.

Creating Your Student Debt Analysis Spreadsheet Template

The cornerstone of any educational debt management strategy is proper analysis. Without visibility into your complete financial picture, you’re essentially flying blind.

Let me walk you through creating what I call the “Educational Financing Command Center”—a comprehensive student debt analysis spreadsheet template that gives you full control over your loan decisions.

Step 1: Inventory All Current and Potential Loans

First things first—you need to document every single loan you have or might consider. Last summer, I worked with a finance student who swore she “only had two loans” until we dug deeper and uncovered a small emergency loan she’d taken from her university during sophomore year. These forgotten loans can wreak havoc on your credit score and overall financial health.

Your spreadsheet should include these columns:

- Loan provider

- Loan type (federal subsidized, unsubsidized, private, etc.)

- Principal amount

- Interest rate

- Loan term

- Deferment options

- Repayment flexibility

- Special conditions or benefits

For potential future loans, create a separate tab using the same structure to compare options before making decisions.

Step 2: Project Your Complete Educational Financing Needs

One of the biggest mistakes I see? Students who plan their educational debt management strategy one semester at a time. This short-sighted approach is like plotting a cross-country road trip by only looking 100 feet ahead.

Instead, create a comprehensive projection that covers your entire educational journey:

- Estimate total education costs through graduation

- Map out all potential funding sources (scholarships, grants, work-study, family contributions)

- Identify the “funding gap” that needs to be covered by loans

- Create a semester-by-semester borrowing plan

My colleague from the financial aid office at State University (who wishes to remain anonymous) once told me, “I can always tell which students will have the most post-graduation financial stress—they’re the ones who show up each semester in crisis mode, surprised by the bill.”

Don’t be that student.

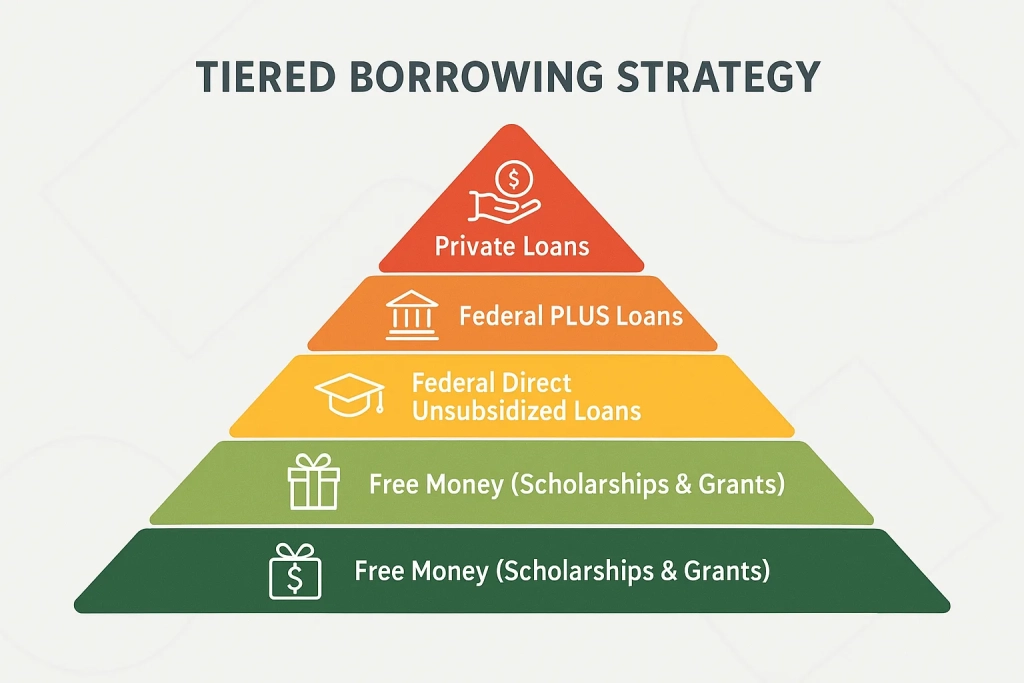

How to Implement a Tiered Finance Student Loan Optimization Technique

Ready for some advanced educational debt management strategy? Let’s talk about tiered borrowing—a loan optimization approach that many finance students understand in theory but rarely apply to their own situations.

What Is Tiered Borrowing?

Tiered borrowing means prioritizing your loan sources based on their overall cost and flexibility, then exhausting each tier before moving to the next. Here’s how I recommend structuring your tiers:

Tier 1: “Free” Money (Scholarships & Grants) This should be obvious, but you’d be shocked how many students don’t maximize these opportunities. My client Amara assumed her partial scholarship would automatically renew each year—until it didn’t because she missed a simple application deadline. Painful lesson.

Tier 2: Federal Direct Subsidized Loans These loans don’t accrue interest while you’re in school, making them significantly cheaper than other options. Max these out before touching anything else.

Tier 3: Federal Direct Unsubsidized Loans The interest starts accumulating immediately, but these still offer valuable flexibility and protection.

Tier 4: Federal PLUS Loans Higher interest rates, but still come with federal protections.

Tier 5: Private Loans from Credit Unions or Banks Your last resort, but sometimes necessary. These require the most careful analysis.

Creating a Strategic Repayment Timeline

An effective educational debt management strategy isn’t just about borrowing—it’s also about planning your repayment approach before you graduate.

Here’s a personal story that illustrates why this matters: in my first advisory role, I worked with a recent finance graduate who had taken on $87,000 in student loans. Smart guy, great job offer, but he’d never created a repayment strategy. When we ran the numbers on standard repayment, he literally turned pale. Had he analyzed this during school, he might have made different choices about his summer internships or part-time work.

Your repayment timeline should include:

- Projected post-graduation salary (be conservative)

- Monthly payment amounts under different repayment plans

- Impact of accelerated payment strategies

- Debt-to-income ratio analysis

Leveraging Your Finance Knowledge for Student Debt Analysis

As a finance student, you have an advantage—you understand concepts like net present value, opportunity cost, and amortization. Use these tools to create a more sophisticated educational debt management strategy.

Applying NPV to Educational Borrowing Decisions

One technique I’ve taught finance students is to use Net Present Value calculations when comparing different loan options or education paths. This approach helps quantify the true cost of each option.

For example, when weighing whether to borrow more to attend a prestigious private university versus a more affordable state school, consider:

- The differential in expected starting salaries

- The total cost difference in loan repayment

- The opportunity cost of delayed higher earnings

Running these numbers through an NPV calculation often produces surprising results. I’ve seen students choose what appeared to be the “expensive” option because the NPV analysis showed it was actually more financially advantageous in the long run. Conversely, I’ve watched students realize that an extra $50,000 in loans for a marginally more prestigious school didn’t make mathematical sense.

Remember—this isn’t just about minimizing debt. It’s about optimizing your overall financial outcome.

Developing Your Educational Loan Comparison Framework

When comparing loan options, most students focus solely on interest rates. But an effective educational loan comparison framework considers multiple factors:

Interest Rate Structure

- Fixed vs. variable rates

- Potential rate changes over time

- Relationship between rate and credit score

Repayment Flexibility

- Available repayment plans

- Hardship deferment options

- Forbearance terms

Forgiveness Potential

- Public Service Loan Forgiveness eligibility

- Income-driven forgiveness provisions

- State-specific forgiveness programs

Protection Features

- Death and disability discharge

- Bankruptcy treatment

- Co-signer release options

A client of mine—let’s call her Jenna—chose a private loan with a 4.8% interest rate over a federal loan at 5.2%, focusing solely on that 0.4% difference. Two years later, when she needed to take a lower-paying job due to family circumstances, she discovered the federal loan would have offered income-based repayment that would have substantially reduced her monthly obligation. That 0.4% “savings” ended up costing her thousands in financial flexibility.

This is why your educational loan comparison framework needs to be comprehensive. The cheapest loan on paper isn’t always the best loan in practice.

Special Considerations for Finance Students

As someone who has advised countless finance students specifically, I’ve noticed some patterns unique to your field:

Industry-Specific Repayment Resources

Many financial firms offer loan repayment assistance as part of their compensation packages. Some even have specific programs for new hires from target schools. Include these potential resources in your educational debt management strategy.

Certification Costs Beyond Your Degree

Finance students often need additional certifications after graduation—CFA, CFP, Series exams, etc. These costs come right when you’re starting loan repayment. Build these expenses into your overall educational financing plan.

I still remember a former client who had carefully planned his student loan repayment only to be blindsided by the costs of CFA preparation and testing. “I feel like I’m back in school, but now I have to pay for everything while working full-time,” he told me, clearly stressed.

Balancing Educational Debt Against Investment Opportunities

Finance students face a unique dilemma upon graduation: should you aggressively pay down student loans or start investing early?

The mathematically optimal answer depends on:

- Your loan interest rates versus expected investment returns

- Your risk tolerance

- Your career stability

- Tax considerations

One approach I often recommend is what I call the “75/25 Split”—put 75% of your available funds toward the highest-interest debt while directing 25% toward retirement investments. This helps you build good investing habits while still making meaningful progress on debt reduction.

Creating Your Own Educational Debt Management Strategy Workbook

Now that we’ve covered the core concepts, let’s put everything together into a comprehensive workbook that will serve as your financial command center throughout your educational journey.

Essential Components of Your Workbook

1. Loan Inventory Dashboard Create a master sheet that tracks all current and potential loans with automatic calculations for total debt, weighted average interest rate, and projected monthly payments.

2. Education Cost Projector Map out all anticipated costs by semester, including tuition increases, housing changes, and other variables.

3. Funding Gap Analysis This sheet identifies exactly how much you’ll need to borrow each period after accounting for scholarships, grants, and other funding sources.

4. Loan Comparison Calculator Build a tool that allows you to compare different loan options using metrics beyond just interest rates.

5. Repayment Simulator Create projections of different repayment strategies and their impact on your post-graduation cash flow.

6. Career Path Financial Projector This advanced sheet helps you model how different career paths might affect your ability to manage your educational debt.

If spreadsheets aren’t your thing (ironic for a finance student, but it happens), there are several student loan planning tools that can help you implement parts of this strategy.

My Personal Educational Debt Management Strategy Story

I’ve walked this path myself. In my early twenties, I had accumulated $63,000 in student loans—a mix of federal and private debt with interest rates ranging from 4.5% to 8.9%. I had the knowledge to manage this effectively but lacked the systematic approach I’m sharing with you today.

The turning point came when my first post-graduation financial planning client turned the tables and asked me about my own debt strategy. I was embarrassed to realize I couldn’t clearly articulate it. That weekend, I built the first version of this educational debt management strategy workbook for myself.

Within 18 months of implementing this system, I had:

- Refinanced my highest-interest private loans, saving $4,200 over the life of the loan

- Qualified for an income-driven repayment plan that better matched my early-career salary

- Created a targeted prepayment strategy focusing on the highest-cost loans first

- Identified a state loan forgiveness program I qualified for by working with underserved communities

The result? I paid off my entire student loan debt in 7 years instead of the projected 15—saving over $18,000 in interest payments. And more importantly, I never felt financially suffocated by my debt because I had a clear plan and visibility into my options.

Conclusion: Your Educational Debt Management Strategy Journey

Student loans are neither inherently good nor bad—they’re simply tools. Like any tool, their value depends on how skillfully you use them. As a finance student, you have both the responsibility and the capability to use these tools with exceptional skill.

The educational debt management strategy workbook I’ve outlined isn’t just about minimizing debt—it’s about optimizing your overall financial outcome. It’s about making intentional decisions rather than reactive ones. It’s about applying the financial principles you’re learning in class to your own life.

Your professors are teaching you how to manage millions of dollars for future employers and clients. Isn’t it worth investing a few hours to manage your own educational financing with the same level of care?

I’d love to hear how you implement these strategies and what results you achieve. After all, your success stories are what make my work meaningful.

Ready to create your own loan analysis workbook and develop a personalized educational debt management strategy? Start by downloading my basic template and customize it to your specific situation.

FAQs About Educational Debt Management Strategy

Is it better to work during school to minimize loans or focus entirely on studies?

This depends on your specific situation. In my experience, moderate part-time work (10-15 hours weekly) often strikes the best balance. I’ve seen students who work too many hours see their grades suffer, potentially harming their job prospects and defeating the purpose. However, I’ve also seen students use strategic summer internships to both build their resumes and significantly reduce borrowing needs. The key is to quantify the trade-off—if working 10 hours weekly at $15/hour reduces your loans by $4,800 annually, is that worth the time commitment?

Should I consolidate my loans after graduation?

Consolidation can simplify repayment by combining multiple loans into a single payment, but it’s not always the best financial decision. Federal loan consolidation generally averages your interest rates, potentially increasing your overall cost. Private refinancing can lower rates but eliminates federal protections. Your optimal strategy depends on your specific loans, career stability, and financial goals. I typically recommend avoiding consolidation until you’ve been in your career for at least 12-18 months to better understand your financial situation.

How does student loan debt affect my ability to buy a home?

Student loans impact your debt-to-income ratio, a key metric lenders use when evaluating mortgage applications. However, many lenders now recognize that educational debt represents an investment in earning potential. If you’re planning to buy a home within 2-3 years of graduation, consider selecting a repayment plan that minimizes your monthly payment (like income-driven options), even if it costs more in the long run. You can always refinance or accelerate payments after securing your mortgage.

Is loan forgiveness a reliable strategy to include in my educational debt management plan?

Loan forgiveness programs can be valuable, but I advise against building your entire strategy around them. Program requirements can change, and many require 5-10 years of qualifying payments before forgiveness. According to the Education Data Initiative, less than 3% of applicants who apply for Public Service Loan Forgiveness have been approved historically. View forgiveness as a potential bonus rather than a guaranteed outcome, and always have a backup plan.

How much should my monthly student loan payment be compared to my starting salary?

Financial advisors traditionally recommend that student loan payments not exceed 8-10% of your gross monthly income. For finance graduates specifically, I typically recommend staying under 12% for the first two years, then accelerating payments as your income grows. To put this in perspective, if your starting salary is $65,000, aim to keep monthly payments under $650-$780. The Consumer Financial Protection Bureau’s repayment calculator can help you estimate affordable payment amounts.

Should I prioritize paying off student loans or building an emergency fund after graduation?

This is one of the most common questions I receive. My recommendation is to build a minimum emergency fund of one month’s expenses before focusing on accelerated loan payments. Then continue building your emergency fund while making regular loan payments until you reach 3-6 months of expenses saved. The Financial Planning Association offers excellent resources on balancing competing financial priorities like these.